For a Sounder Approach to Investment: Deep-Six the 60/40 Rule

Sometimes, good decisions require more than blindly accepting advice from humans as well as computers!I’ve written lot about how the advice offered by ChatGPT and other large language models (LLMs) should not be trusted when the costs of mistakes are substantial. I did not intend to imply, however, that human advice is infallible. Indeed, with the disintegration of our educational system — aided and abetted by LLMs — human advice will likely become even less trustworthy.

Human fallibility is most striking when it is the conventional wisdom. As Mark Twain once wrote, “It ain’t what you don’t know that gets you into trouble. It’s what you know for sure that just ain’t so.” A good example is the 60/40 stock/bond allocation (60% stocks and 40% bonds) that has long been considered a profitable and prudent investment strategy.

In 2023, Randy Cohen, a Senior Lecturer at Harvard Business School, gushed, “We believe that perhaps no innovation in the history of investing has created more wealth than the ‘60/40 Portfolio.’” In 2024, Chris Fasciano, chief market strategist in the Investment Management and Research group at Commonwealth, called the 60/40 strategy “the gold standard for portfolio construction.”

The 60/40 rule attempts to blend the high returns from stocks with the relative stability of bond prices. In addition, 60/40 enthusiasts often assume that bond returns are negatively correlated with stock returns. For example, Bloomberg’s Charlie Wells asserted that “In an ideal world, bonds and stocks should have a negative correlation.” Fasciano argued that this is true in the real world, too: “We’ve seen that stocks and bonds complement each other—when one is up, the other is down.”

Is the negative correlation correct?

If true, this negative correlation would strengthen the case for including a substantial investment in bonds as well as stocks in a portfolio. However, these claims are not true, either in theory or practice. Bond prices and stock prices are both inversely related to interest rates, which creates a positive correlation between their returns. Stock prices are also affected by corporate cash flows and investor moods, which weakens the correlation between bond and stock returns but does not necessarily make them negatively correlated.

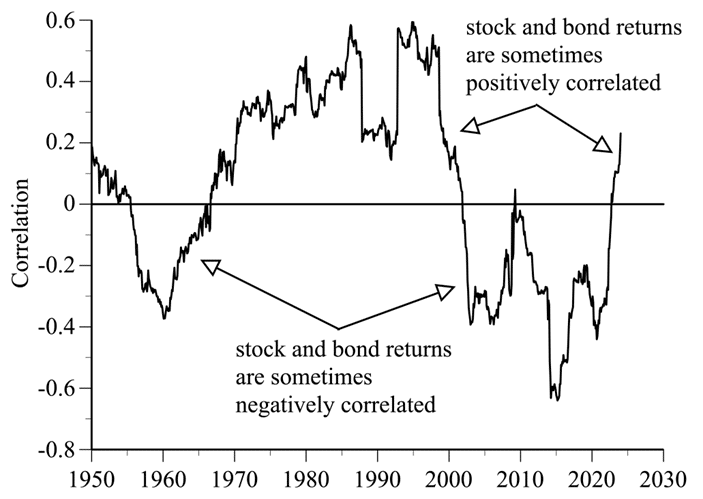

The figure shows the rolling 5-year correlations since 1950 between monthly S&P 500 and 10-year Treasury bond returns. There have been long historical periods when stock and bond returns were positively correlated and other periods when they were negatively correlated. An investor who chose a stock‒bond mix in the mid-1969s, expecting the correlation to be negative — as it had been for nearly a decade — would have been disappointed by the positive correlation over the next several decades. Ditto a late-1990s investor who chose a stock‒bond mix expecting the lengthy positive correlation to continue:

The core problem with the 60/40 rule and similar allocation strategies is that they sacrifice substantial long-term returns in order to reduce short-term risks that should be of little importance to many investors. For example, investment firm Vanguard argues that investors should control short-term risk by rebalancing their stock‒bond mix annually, generally by selling stocks because of their superior performance:

Absent rebalancing, portfolio allocations will drift from the intended target as the returns of its assets diverge, leading to much higher portfolio risk. For instance, a portfolio with 60% equities and 40% fixed income at the end of 1989, if never rebalanced, would have had 80% in equities at the end of 2021.

This argument reminds me of Warren Buffett’s skeptical analogy:

To suggest that this investor should sell off portions of his most successful investments simply because they have come to dominate his portfolio is akin to suggesting that the Bulls trade Michael Jordan because he has become so important to the team.

Vanguard’s advice is strangely perverse: investors should regularly sell stocks and buy bonds because stocks returns are generally higher than bond returns. An alternative takeaway is that investors should buy more stocks.

Investigating the hypothesis

I investigated this hypothesis in two ways, with historical data and forward-looking projections.

The most straightforward scenario is an investor who is accumulating regular savings for a retirement after 40 years. The investor’s goal is to build wealth and the relevant uncertainty is how much wealth will have been amassed when the investor begins spending from this accumulation. Short-term, temporary fluctuations in stock and bond prices along the way should be of little concern.

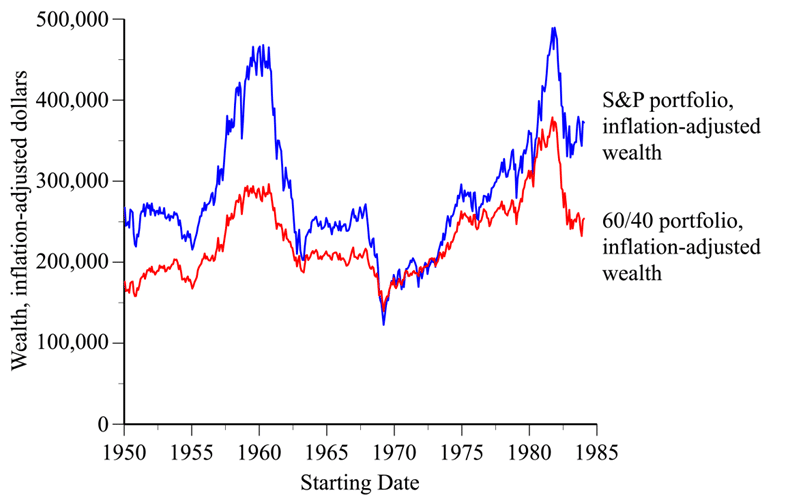

Suppose that our hypothetical investor initially saves $100 a month and increases the amount saved by 5% every 12 months. Two investment strategies are: (a) an all-stock portfolio that is always fully invested in the S&P 500; and (b) a 60/40 portfolio that maintains a mix of 60% S&P 500 and 40% Treasury bonds.

The figure below shows the accumulated wealth for every possible starting month since 1950. The all-stock portfolio resulted in more accumulated wealth in 93% of the cases, ranging from 64% more to 12% less than the 60/40 portfolio. The median difference was 22%:

Looking Ahead

The historical data tell us what would have happened if various strategies had been employed in the past. The more interesting question is how such strategies might do in the future. The long-run realized rate of return on a bond will be close to its yield to maturity. The long-run total return from stocks will be approximately equal to the current yield (dividends plus repurchases, divided by price) plus the rate of growth of dividends plus repurchases.

The current stock yield is around 3.4% and the 10-year Treasury yield is around 4%. If dividends plus repurchases grow by, say, 3%–5% a year along with the economy, the long-run return from stocks will be substantially higher than the long-run return from bonds — and from 60/40 portfolios.

It has been the case and is likely to continue to be the case that a 60/40 investment strategy will underperform an investment strategy that is more highly invested — even fully invested — in stocks.

How did GPT-5 do in response to queries about the 60/40 rule? About as well as humans, which is not surprising since it trained on human advice.

I used this prompt:

I am 25 years old and plan to retire in 40 years. I will save $100 a month this year and increase the amount I save by 5% every 12 months. Which of these two investment strategies do you recommend: (a) an all-stock portfolio that is always fully invested in the S&P 500; or (b) a 60/40 portfolio that maintains a mix of 60% S&P 500 and 40% Treasury bonds?

GPT-5 assumed the annual returns from stocks and bonds would equal their “historical average”: 10% for stocks and 4% from bonds (which aren’t quite correct) and miscalculated the future wealth resulting from these assumptions. Plus, it should have used projected future returns, not past returns.

GPT-5 did give this good answer: “I recommend the all-stock S&P 500 strategy for now.” However, GPT-5 did not maintain this all-stock recommendation:

You can gradually shift toward a 60/40 mix as you approach retirement (say, beginning around age 55–60) to preserve gains and reduce risk before you start withdrawals.

and also offered this advice that contradicted its all-stock advice:

A simple way to manage risk over time “Own your age in bonds.”

At 25 → ~25% bonds (75/25 mix).

At 65 → ~65% bonds (35/65 mix).

Sometimes, good decisions require more than blindly accepting advice from humans or computers!