Investor, AI Isn’t Your Big Fix

In investing and elsewhere, an AI label is often more effective for marketing than for performanceAn exchange-traded fund (ETF) is a bundle of securities, like a mutual fund, that is traded on the New York Stock Exchange or other exchanges, like an ordinary stock. There is now nearly $5 trillion invested in 5,000 ETFs.

One attractive feature of ETFs is that, unlike shares in typical mutual funds, which can only be purchased or sold after the markets close each day, ETFs can be traded continuously while the markets are open. This evidently appeals to investors who think that they can jump in and out of the market nimbly, buying before prices go up and selling before prices go down. Unfortunately, day trading takes a lot of time and the results are often disappointing. Perhaps computers can do better?

In 2017 the Association of National Advertisers chose “AI” as the Marketing Word of the Year.

In October of that year, a company with the cool name Equbot launched AIEQ, which was touted as the first ETF run by artificial intelligence (AI). And not just any AI, but AI using Watson, IBM’s powerful computer system that had defeated the best human players at Jeopardy.

Watson’s Jeopardy win was stunning but the ability to search a database for facts and use a lightning-fast electronic finger to push a button don’t have much to do with predicting whether the price of Apple stock is about to go up or down. Stock prices are buffeted wildly by news events (which are, by definition, unpredictable; otherwise they wouldn’t be news!) and by human emotions (which are, by nature, volatile and unpredictable). Many an investor and computer has found it easy to find patterns and relationships in historical data that turn out to be coincidental and fleeting. Backtesting the past is very different from predicting the future.

Equbot boasts that AIEQ is “the ground-breaking application of three forms of AI”: genetic algorithms, fuzzy logic, and adaptive tuning. Investors may not know what any of these words mean but that is part of the allure. If someone says something we don’t understand, it is natural to think that that person is smarter than we are. Sometimes, however, mysterious words and cryptic phrases are meant to impress, not inform.

Chida Khatua, CEO and co-founder of EquBot, used ordinary English but was still vague about the details: “EquBot AI Technology with Watson has the ability to mimic an army of equity research analysts working around the clock, 365 days a year, while removing human error and bias from the process.” I remember Warren Buffett’s advice to never invest in something you don’t understand. I also acknowledge that it would be nice to remove human error and bias (is anyone in favor of error and bias?). But computers looking for patterns have errors and biases too.

Computer algorithms for screening job applicants, pricing car insurance, approving loan applications, and determining prison sentences have all been found to have significant errors and biases, due not to programmer biases but the nature of patterns. For example, an Amazon algorithm for evaluating job applicants discriminated against women who had gone to women’s colleges or belonged to women’s organizations because there were few women in the algorithm’s database of current employees. An Admiral Insurance algorithm for setting car insurance rates was based on an applicant’s Facebook posts. One example the company cited was whether a person liked Michael Jordan or Leonard Cohen which humans would recognize as a decision-making tool ripe with errors and biases.

Admiral said that its algorithm “is constantly changing with new evidence that we obtain from the data. As such our calculations reflect how drivers generally behave on social media, and how predictive that is, as opposed to fixed assumptions about what a safe driver may look like.”

This claim was intended to show that their algorithm is flexible and innovative. What it actually reveals is that their algorithm can find historical patterns but not that it can find useful predictors. The algorithm changes constantly because it has no logical basis and is continuously buffeted by short-lived correlations.

Algorithms based on patterns are inherently prone to discover meaningless coincidences that human wisdom and common sense would recognize as such. Taking humans completely out of the process and hiding the mindless pattern discovery inside an inscrutable AI black box is not likely to end well.

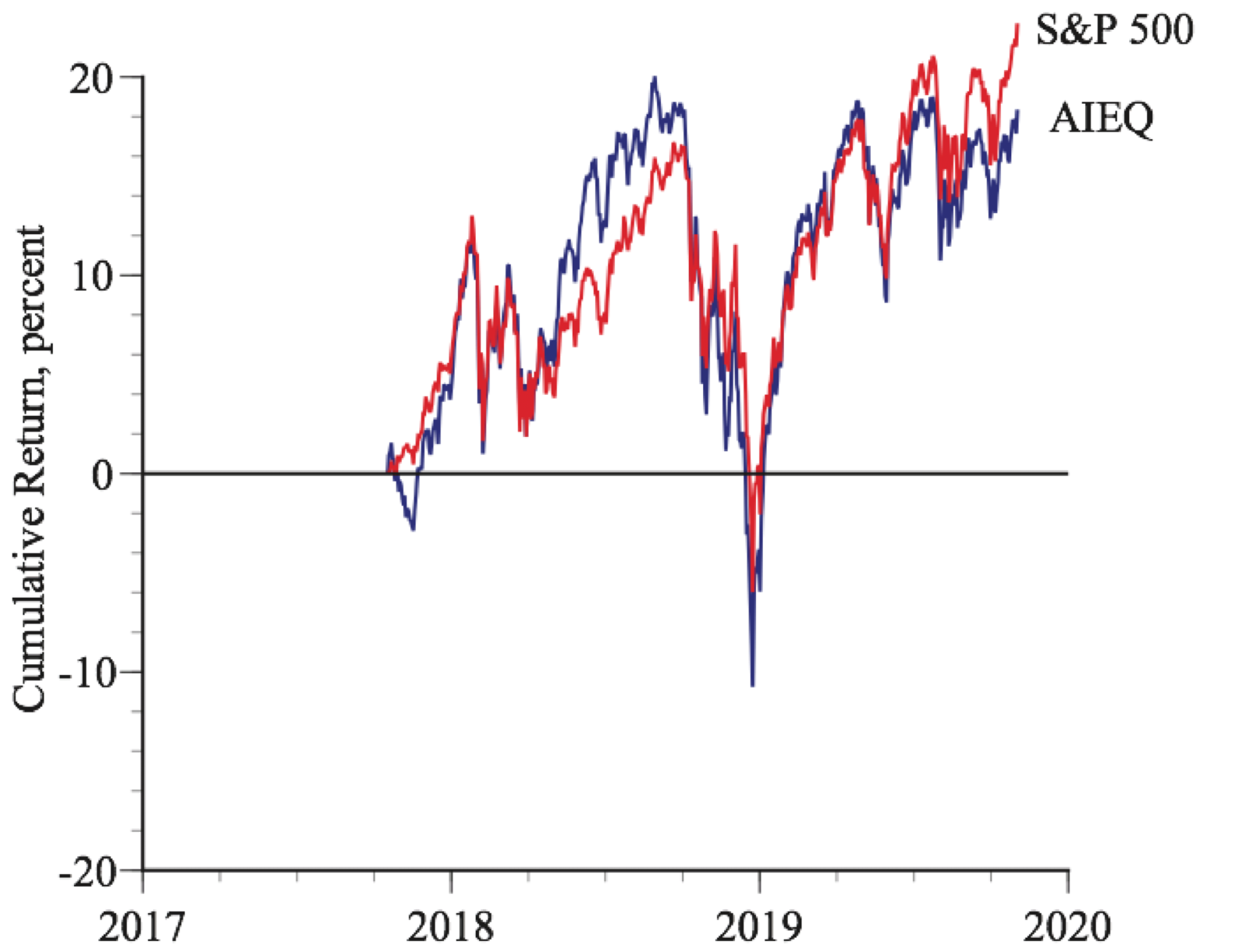

Figure 1 shows how AIEQ worked out. Despite the promises of genetic algorithms, fuzzy logic, and adaptive tuning, AIEQ seems to be a “closet indexer,” tracking the S&P 500 while underperforming it. From inception through November 1, 2019, AIEQ had a cumulative return of 18 percent, compared to 23 percent for the S&P 500. Meanwhile, investors paid a 0.77 percent annual management fee for this distinctly mediocre performance.

Figure 1 Underwhelming Performance

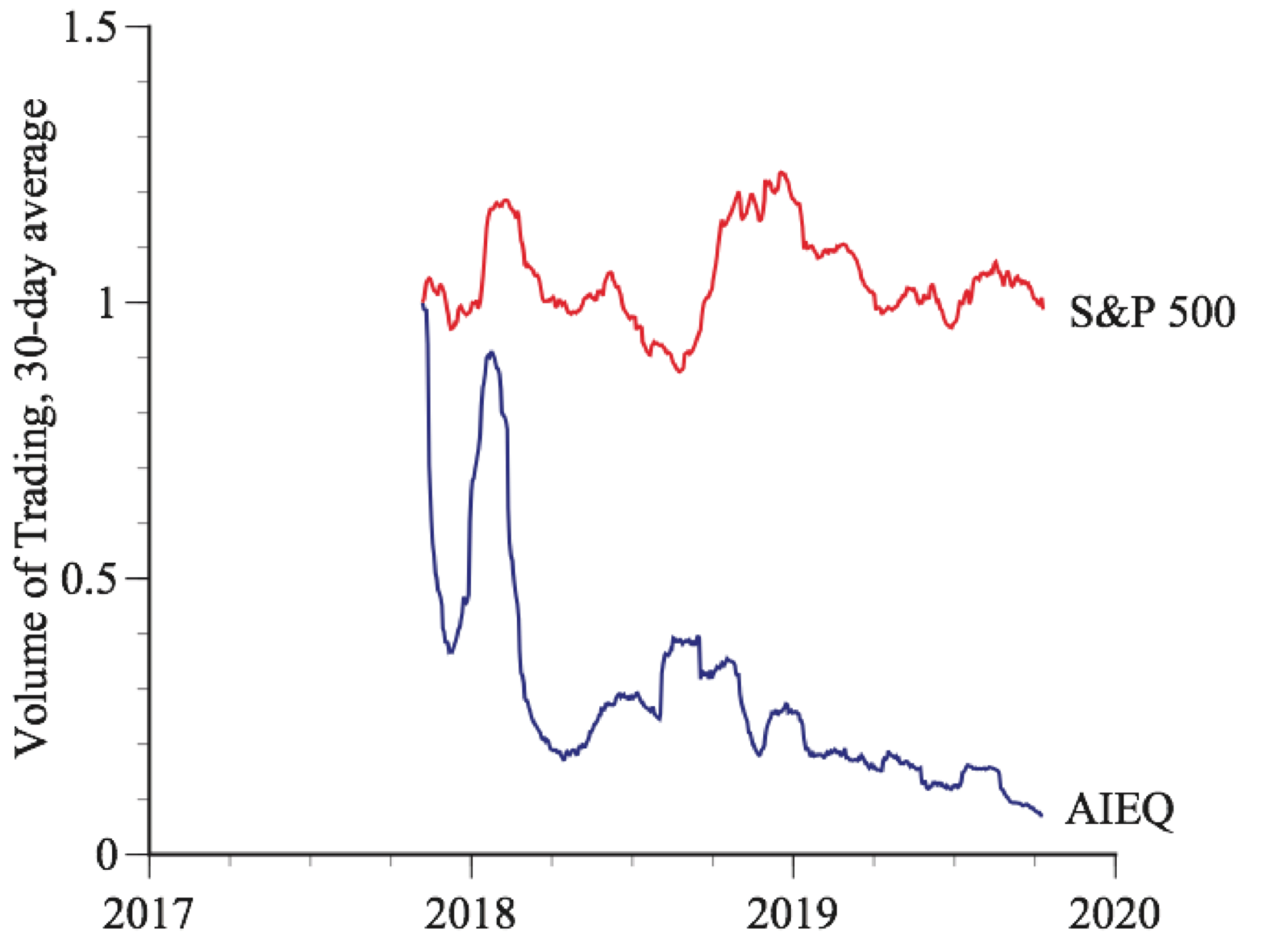

Figure 2 compares the volume of trading in AIEQ to the volume of trading in the S&P 500, both scaled to equal 1 when AEIQ was launched. Once the disappointing results become apparent, customers lost interest.

Figure 2 Overwhelming Disinterest

In investing and elsewhere, an AI label is often more effective for marketing than for performance.

If you enjoyed this discussion, don’t miss Prof. Gary Smith’s analysis of the difference a stock ticker name makes in “A BABY, A GEEK, and a COW” all walk into a bar…

Also: We see the pattern! But is it real? It’s natural to imagine that a deep significance underlies coincidences. Unfortunately, patterns are not always a source of information. Often, they are a meaningless coincidence like the 7-11 babies this summer. (Gary Smith)