A BABY, a GEEK, and a COW…

… all walk into a bar looking for some BEER and VINO…When stocks are traded, they are identified by ticker symbols (so-called because trading was once reported on ticker tape machines). Companies have traditionally chosen abbreviations of their names for their tickers; for example, AAPL for Apple and GOOG for Google. Sometimes the companies’ ticker symbols become much more familiar than their names. Think of International Business Machines (ticker: IBM). Minnesota Mining and Manufacturing (ticker: MMM) ended up changing its legal name to 3M in 2002.

The photo is of women hired to mind the tickers and stock exchange boards at the Waldorf-Astoria, in order to release men for service in World War I. Dated 11-12-1918. US National Archives and Records Administration, catalogued under the National Archives Identifier (NAID) 533759.

The photo is of women hired to mind the tickers and stock exchange boards at the Waldorf-Astoria, in order to release men for service in World War I. Dated 11-12-1918. US National Archives and Records Administration, catalogued under the National Archives Identifier (NAID) 533759.But during the past few decades, dozens of companies have shunned the traditional name-abbreviation convention, choosing ticker symbols that are memorable for their cheeky cleverness. Southwest Airlines chose LUV as a ticker symbol because its headquarters are at Love Field in Dallas and Southwest wanted to brand itself as an airline “built on love.” Other clever tickers are Explosive Fabricators (BOOM), Asia Tigers Fund (GRR), and Tricon Global Restaurants (YUM).

Those inhabitants of cloud cuckoo land who believe that the stock market is “efficient,” in the sense that stock prices accurately reflect true values, dismiss the idea that prices might be affected by anything as superficial as ticker symbols. However, in the real world, investors are not always as rational as efficient-market enthusiasts assume and stock prices are not always “correct.”

Our understanding of human memory suggests that if a ticker is easy to pronounce or clever, it is more memorable and likely to evoke positive feelings. That may lead investors to remember the stock and be more confident that the company is a good investment. Clever tickers may harness the power of branding, making an emotional connection with customers by nurturing a memorable word in their minds.

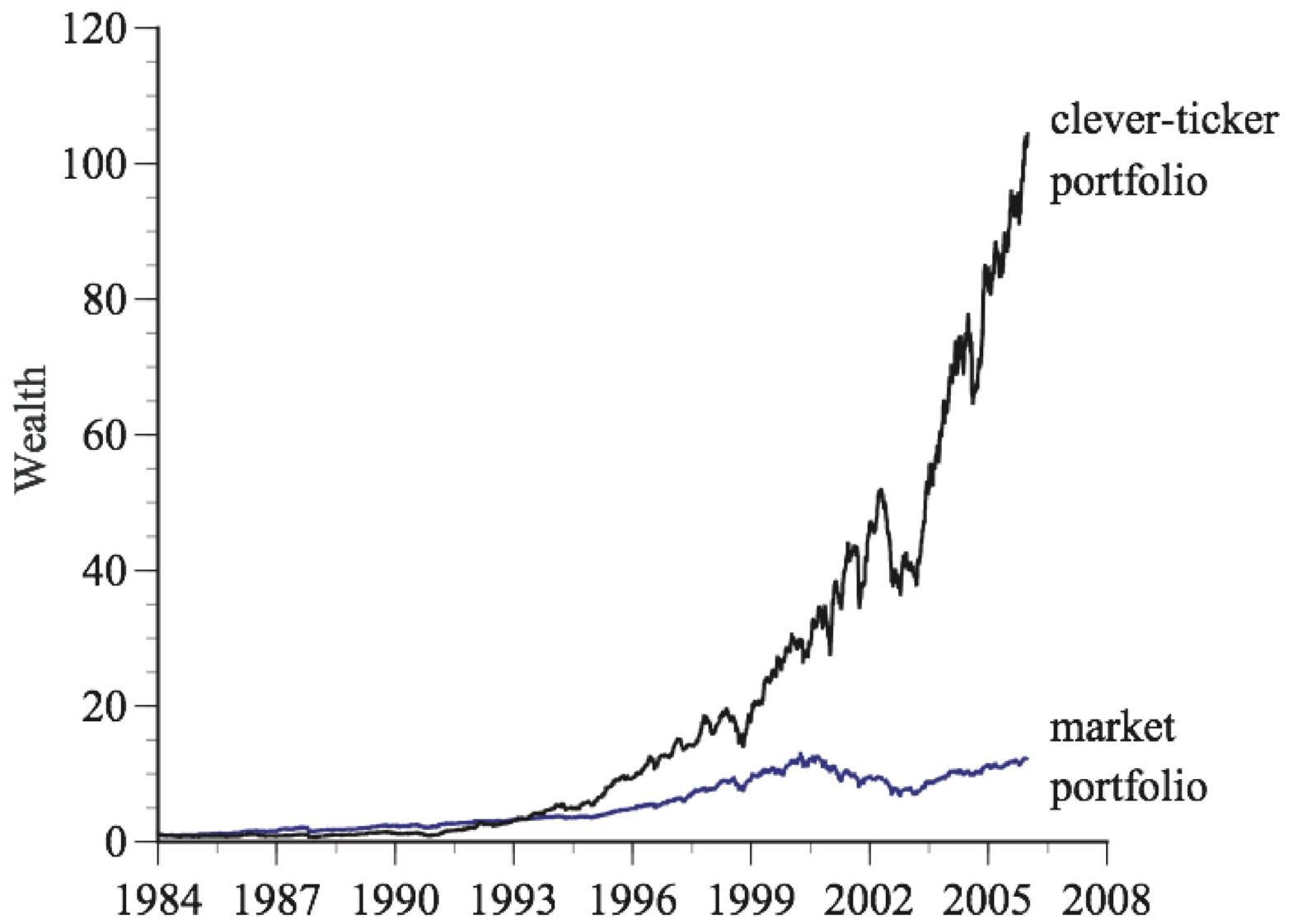

To test this possibility, I did a study with two Pomona students in 2006 that compared a portfolio of stocks with clever ticker symbols to the overall market over the years 1984 to 2005. I hadn’t expected to find much. I was mistaken. The clever-ticker portfolio soared, with a 24 percent compound annual return compared to 12 percent for the market portfolio. Figure 1 shows that, because of the power of compound interest over this 22-year period, $1 invested in the market would have grown to $12.17, while $1 invested in the clever-ticker portfolio would have grown to $104.69.

The market-beating performance was not because the clever-ticker stocks were concentrated in a single industry. The 82 clever-ticker companies span 31 of the 81 industry categories used by the U. S. government, with the highest concentration being 8 companies in eating and drinking establishments, of which 4 beat the market and 4 did not. Nor was the clever-ticker portfolio’s success due to the extraordinary performance of a small number of clever-ticker stocks: 65 percent of the clever-ticker stocks beat the market.

Figure 1: The Clever Ticker Portfolio 1984–2005:

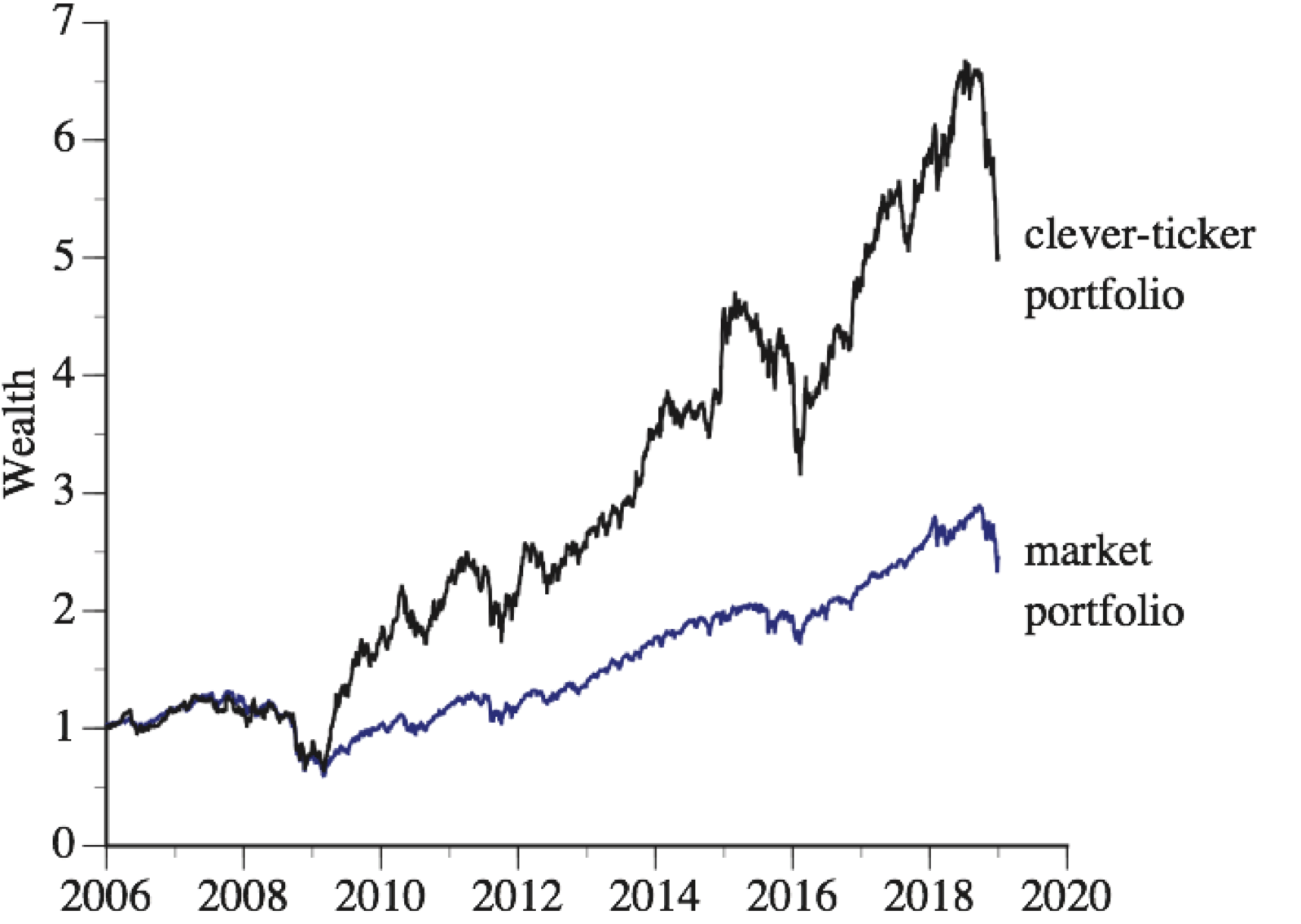

Now, more than a dozen years later, I have revisited this question with two new Pomona students. We looked at the performance of the original clever-ticker stocks during the subsequent 13-year period 2006–2018. Figure 2 shows that, as was true for the original 22 years of data, the clever-ticker portfolio outperformed the market portfolio by a substantial margin.

Starting with $1 on the first trading day in 2006, the market portfolio grew to $1.86 at the end of 2018, a 5 percent compounded annual return, while the clever-ticker portfolio grew to $5.03, a 13 percent annual return. Again, the superior performance of the clever-ticker portfolio was not due to the outstanding performance of a few stocks: 19 of the 22 clever-ticker stocks did better than the overall market.

For the entire 35-year period, the clever-ticker portfolio had a 20 percent annual return, and grew $1 to $526, while the market had a 9 percent annual return and grew $1 to $23.

Investors are human after all. We are able to think logically and critically, but we have feelings and emotions, too. We make mistakes and we are sometimes buffeted by fear and greed, which is good. Think how boring we and our lives would be otherwise.

Figure 2: The Clever Ticker Portfolio 2006–2018:

By an odd coincidence, I was contacted by a former student, Michael Solomon, after the initial study was published. In 2000, Michael was working for Leonard Green, a private equity investment firm, when it acquired VCA Antech, a company that operates a network of animal hospitals and diagnostic laboratories. Leonard Green reorganized VCA Antech and made a public stock offering in 2001. Michael suggested the ticker symbol WOOF and they went with it.

Over the 16-plus years that VCA Antech traded under the ticker symbol WOOF, until it was acquired by Mars, the annual return on its stock was 19 percent, compared to 7 percent for the S&P 500.

Woof! Woof!

If you enjoyed this piece, you might also like: We see the pattern! But is it real? It’s natural to imagine that a deep significance underlies coincidences. Unfortunately, patterns are not always a source of information. Often, they are a meaningless coincidence like the 7-11 babies this summer. (Gary Smith)

Note: The photo is of women hired to mind the tickers and stock exchange boards at the Waldorf-Astoria, in order to release men for service in World War I. Dated 11-12-1918. US National Archives and Records Administration cataloged under the National Archives Identifier (NAID) 533759.