Is Rationality Finally Emerging for Unicorn Share Prices?

Share prices are falling as losses continue to mount2021 was a great year globally for venture capital and startups. Initial public offerings (IPOs) raised a record $594 billion in 2021 globally while VC funding is on track to hit a record $454 billion invested through the first three quarters of 2021.This is up from $332 billion for the first three quarters of 2020, which was the previous record for three quarters.

U.S. startups also did well with big increases in both VC funding and IPOs in 2021. Almost $100 billion of funding was given to startups in the first three quarters while for the full year, there were 416 IPOs, of which 128 were from the tech section. The total amount raised was $156 billion, of which $69 billion was for the tech sector.

On the other hand, share prices are falling driven by the fear of rising interest rates while quietly in the background losses continue to mount. Shares of publicly traded Unicorns dropped between 30% and 90% in the last year. The declines have accelerated in 2022, and the number of articles warning of a meltdown have reached their highest point in years.

While many people are aware that today’s startups are unprofitable, it is the steady accumulation of losses over many years that will likely pose the largest problems to their future and the future of the startup industry and technological innovation in general. As these cumulative losses mount, the chances of startups erasing them becomes more unlikely each year.

Startups that went public in 2021 through SPACs (special purpose acquisition companies) have particularly large losses because many of them have not just losses, but also few if no revenues. How can such a company expect to cover its cumulative losses if it not only does not have profits, it also does not have revenues that might generate profits in the future?

Of American startups going public in 2021, three of them (WeWork, Rivian, and Robin Hood) have more than $3 billion in cumulative losses, a figure first achieved by Amazon more than 15 years ago, bringing the current total to ten. The biggest losses are for Uber ($24.5 billion), WeWork ($12.2 billion), Snap ($8.4 billion), Lyft ($8.0 billion), and Airbnb ($6.4 billion), followed by Nutanix, Rivian, RobinHood and Bloom Energy.

More publicly traded ex-Unicorn startups also passed the $1 billion and $500 million mark in cumulative losses. Of the 133 publicly traded ex-Unicorn startups that I analyzed, 23 now have greater than $1 billion in cumulative losses and another 36 have greater than $500 million. This means that 69 of the 133 ex-Unicorns, or more than half, have greater than $500 million in cumulative losses.

A more revealing figure might be the number of ex-Unicorns with cumulative losses greater than annual revenues, a feat briefly achieved by Amazon when its cumulative losses peaked at $3 billion. There are now 89 of those ex-Unicorns among the total of 133, or about 67%, up from 60% before the IPOs of 2021 are added. This rising percentage partly comes from the many SPACs that had little or no revenues. It’s easy to have cumulative losses larger than revenues when you have no revenues.

Similar problems exist outside the U.S., with many ex-Unicorns having similarly large cumulative losses in China, India, and Singapore. Video-streaming Kuaishou has the largest cumulative losses of any ex-Unicorn as of mid-2021 with $34.7 billion, about 50% higher than those for Uber. Many others have cumulative losses higher than their 2020 revenues.

Consider for a moment the plight of those startups with cumulative losses greater than 2020 revenues. Even if they were to magically achieve profits equal to 10 percent of revenue – a truly difficult feat – it would still take 10 years to erase the cumulative losses. Although Amazon managed to achieve this and later become one of America’s most valuable companies, few startups will likely repeat Amazon’s success, particularly when many of these 89 ex-Unicorns cited above have cumulative losses much greater than their annual revenues.

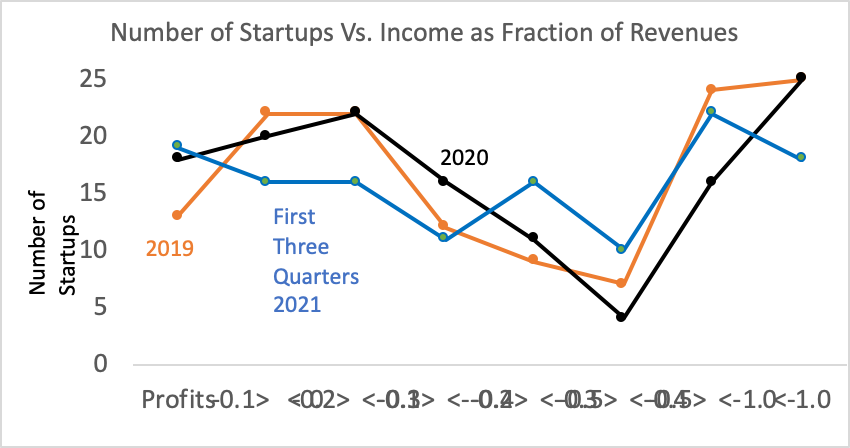

The good news is that the percentage of profitable ex-Unicorns has risen slightly over the last few years. As shown in the below figure, 19 of them were profitable in the first three quarters of 2021, up from 18 in 2020 and 13 in 2019. Nevertheless, there were fewer Unicorn startups with losses less than either 10% or 20% of revenues in 2021 than in 2019 or 2020. Clearly, a trend towards stronger profitability is fairly weak.

The biggest winners were Moderna and Coinbase. Moderna had profits of $7.3 billion on revenues of $11.3 billion in the first three quarters of 2021 largely thanks to the success of its vaccine, although many refuse to be jabbed by them. Coinbase also did well with $2.8 billion in profits on revenues of $5.3 billion thanks to the popularity of cryptocurrencies in 2021, whose prices have fallen by almost 50% in the last three months. Other ex-Unicorns with profits greater than 20% of revenues include video communication provider Zoom, e-commerce seller Etsy, and dating app Bumble whose share prices have also fallen precipitously over the last few months. Even among the most successful of Unicorn startups, positive stories are hard to find.

The continued losses for many startups will continue to worry U.S. (and Chinese) stock markets. These declines have also impacted emerging technology funds such as Ark Innovation ETF, run by Cathie Wood, still America’s most popular advisor on investments. The fund is down 20% in 2022 after being down 30% in 2021, and continued losses will likely put further pressure on the fund’s share price.

One question is how many more publicly traded Unicorns will become profitable in 2022. Although the above figure suggests that the number of profitable ex-Unicorns will likely rise in the coming years, it also suggests this will occur slowly and thus impact only a small number of them in 2022 or 2023. Continued downward pressure on their share prices, and on those startups going public in 2022, is likely as fears of higher interest rates increase and as rationality returns.