Inflation Is the Least of Our Worries!

Yet some fear that the inflation dragon is about to roarThe Federal Reserve (the Fed) can throw the economy into a recession whenever it feels that it is in our best interests to be unemployed — typically because the Fed is convinced that an unruly inflation needs to be tamed by the discipline of unemployment.

For example, in 1979, as the rate of inflation peaked above 13 percent, the Fed moved to make borrowing prohibitively expensive. When Fed Chair Paul Volcker was asked if the Fed’s policies would cause a recession, he replied, “Yes, and the sooner the better.” Interest rates reached 18 percent on home mortgages and were even higher for most other bank loans.

Households and businesses cut back on their borrowing and spending and the unemployment rate topped 10 percent in 1982, the highest level since the Great Depression. But the Fed achieved its single-minded objective as the rate of inflation fell below 4 percent.

At other times, the Fed turns on the monetary spigots in order to help the economy. During the Great Recession that began in the United States in 2007, the Fed pumped billions of dollars into a deflating economy. They are doing the same during the current COVID-19 recession.

Where does this money come from? The total amount of government money outstanding (called the monetary base) includes currency held by the public outside banks and reserves held by banks in their vaults or Fed accounts. The Fed increases the monetary base when it purchases Treasury bonds and other securities from banks and pays for them by crediting the banks with increased reserves. The Fed reduces the monetary base when it sells securities and reduces the reserves of the banks buying the securities.

The Fed more than doubled the monetary base in 2008, from $800 billion in January 2008 to $1.7 trillion in January 2009. Since then, the Fed has tripled the monetary base, to $5.1 trillion, leading some to fear that hyperinflation is on the horizon. When I wrote a few weeks ago that, “Faced with a credit crunch that threatened to pull the economy into a second Great Depression, the government did the right thing by pumping billions of dollars into a deflating economy,” I received several e-mails reminding me of Nobel Laureate Milton Friedman’s warning that, “Inflation is always and everywhere a monetary phenomenon.” Yet, the average annual rate of inflation over the past dozen years has been only 1.7 percent. Why hasn’t the monetary firehose awakened the inflationary dragon?

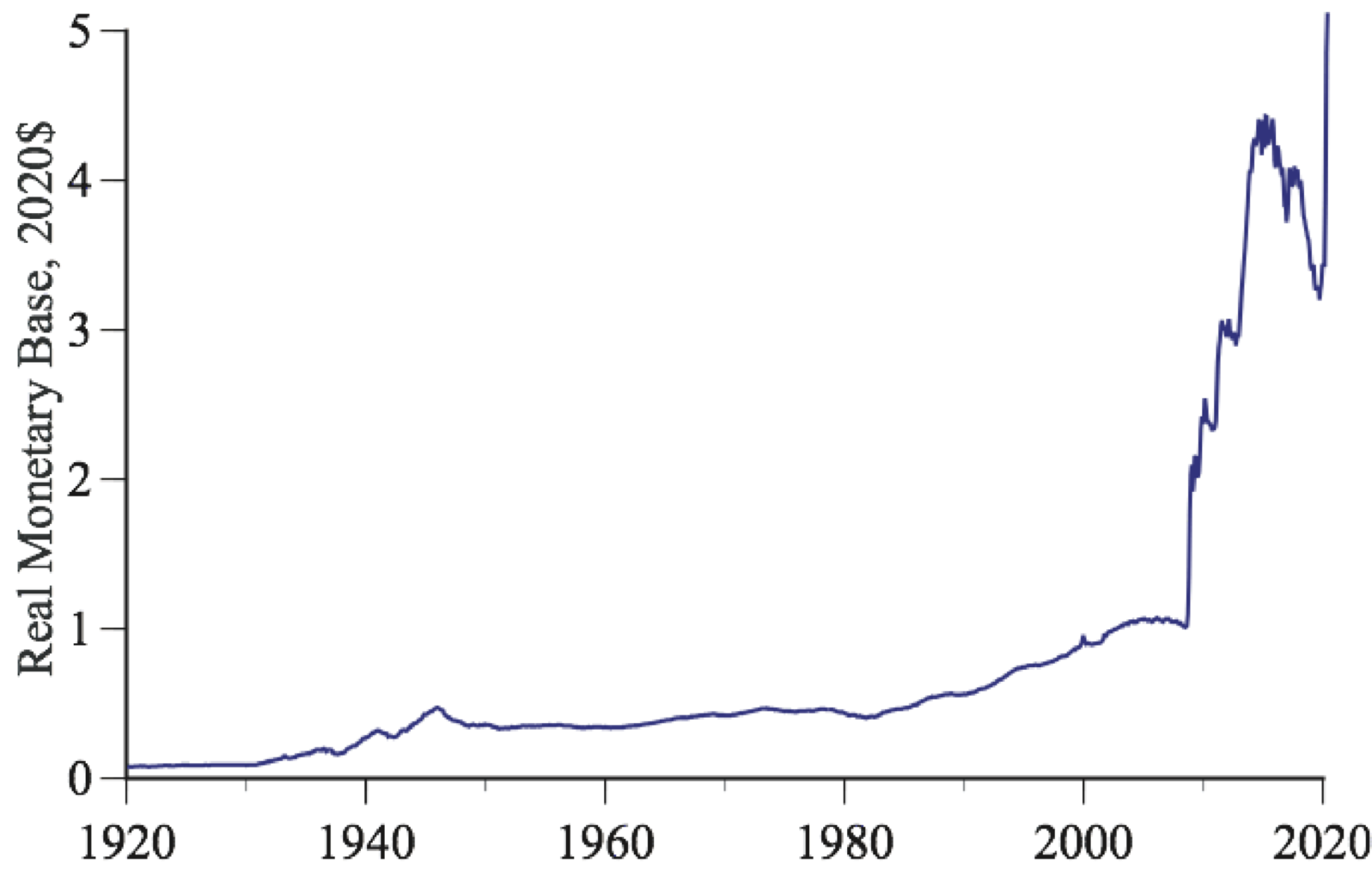

The link between money and inflation is far more tenuous than suggested by Friedman’s pithy remark. Figure 1 shows the real, inflation-adjusted monetary base over the past 100 years. The monetary base has generally increased somewhat faster than consumer prices; since 2007, the monetary base has exploded with little increase in prices, causing the real monetary base to spike upward.

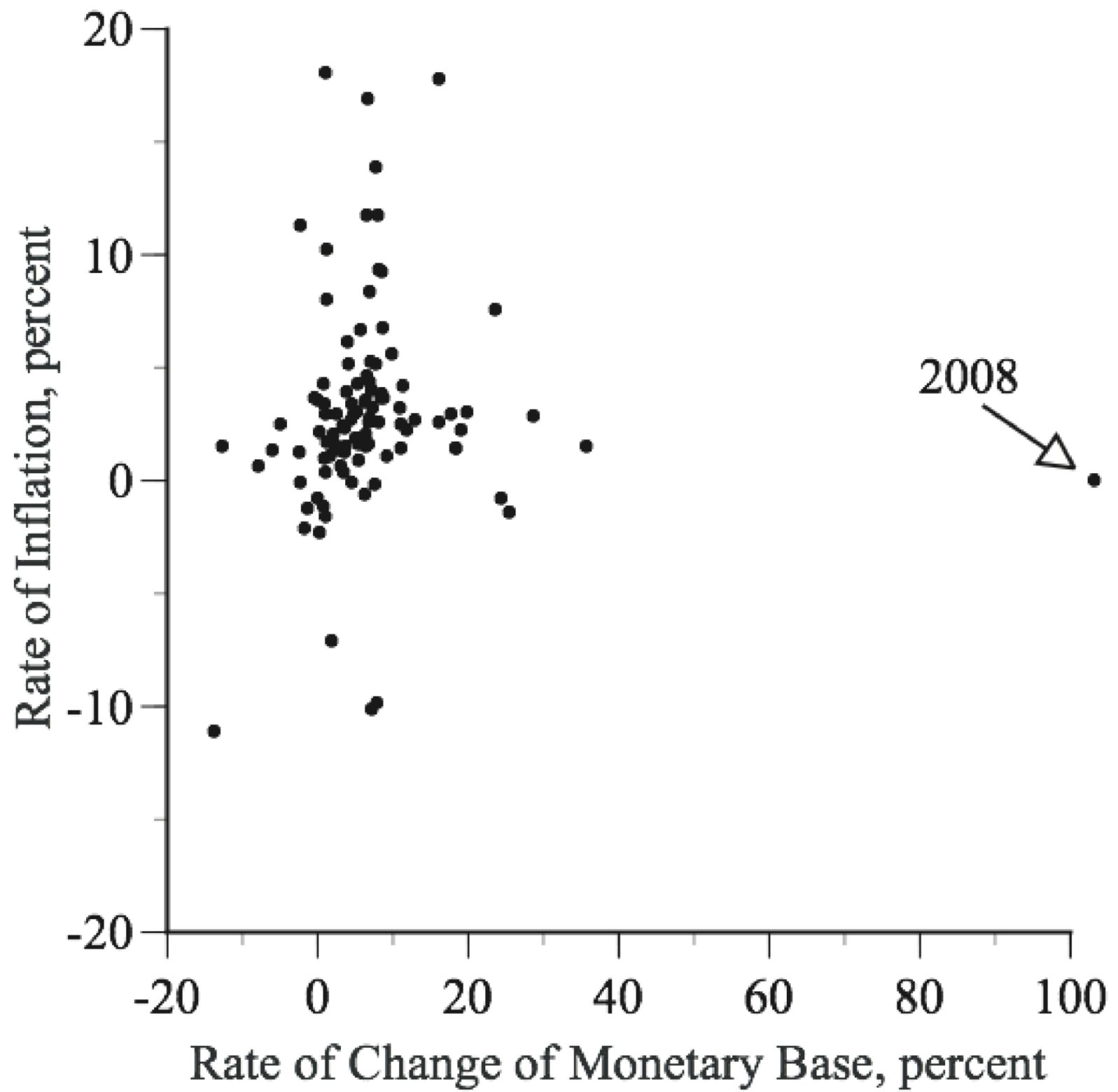

The weak link between money and inflation predates 2008. Figure 2 shows that the correlation between annual changes in the monetary base and the rate of inflation since 1920 has been a minuscule 0.04.

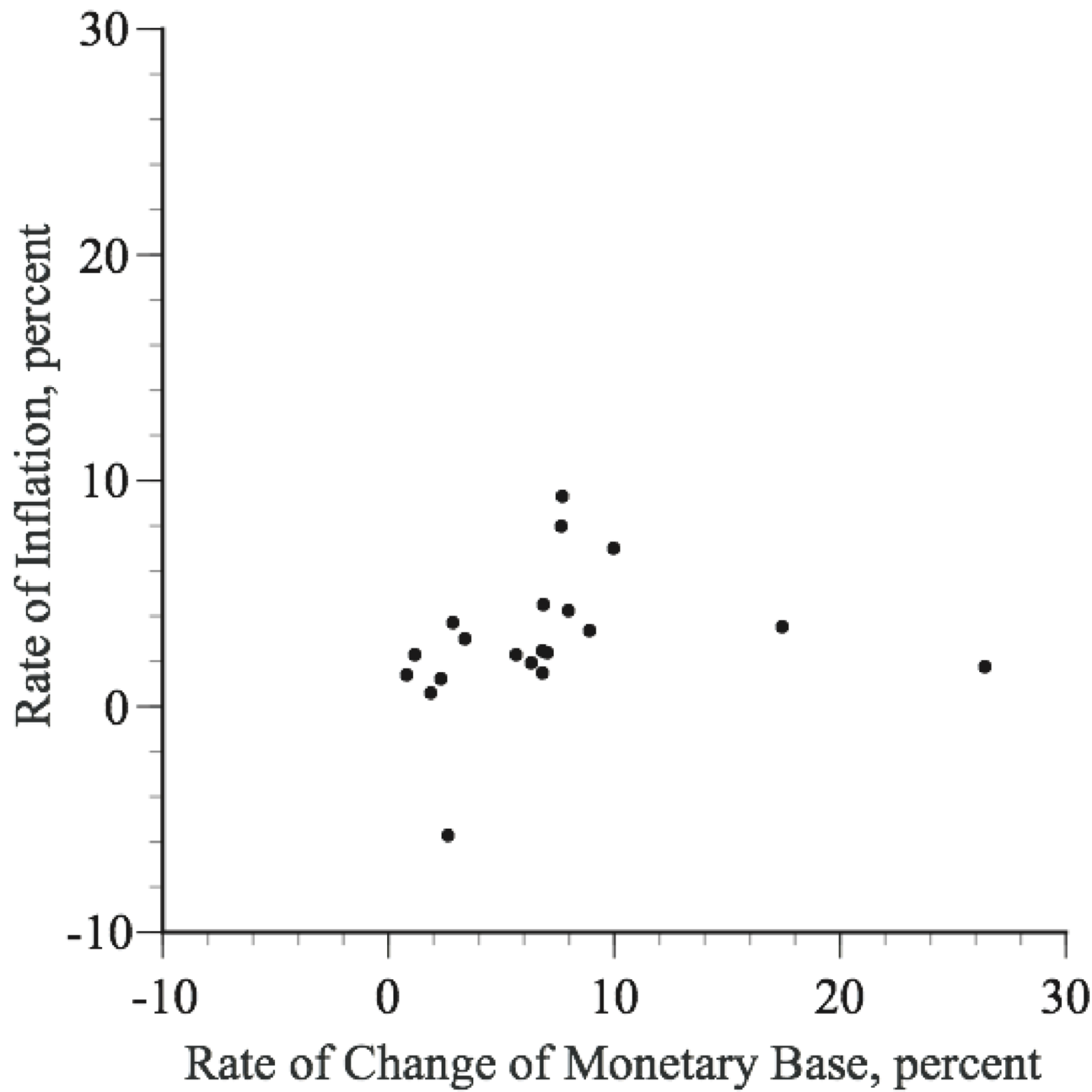

Perhaps it takes more than a year to awaken a sleeping dragon? Figure 3 looks at non-overlapping 5-year periods over the past 100 years and shows only a 0.07 correlation. If I were to tell you that the monetary base had increased at a 7% annual rate over the past year or several years, would you be able to give a reliable estimate of the rate of inflation?

In a market economy, prices depend on the relationship between demand and supply and on institutional factors, such as state commissions that regulate public utilities. The monetary base affects prices to the extent that it affects the demand for various goods and services, but other factors affect demand, too. Supply also matters and in our increasingly global economy, demand and supply can come from anywhere in the world. U. S. manufacturers can’t charge $20 for something that can be produced in India, Indonesia, or Ireland for $10.

Two Tsunamis

If this weren’t enough, two economic tsunamis preclude any simple relationship between money and inflation: the role of the dollar as world money and the diminished importance of bank deposits and loans.

The U.S. dollar is the official currency in several countries and an unofficial medium of exchange in many others. Somewhere between one-half and two-thirds of all U. S. currency is now held outside the United States. U.S. dollars flowing through world markets may well affect world prices, but the effects are diluted because these dollars are a relatively small part of the total world money supply.

The second tsunami is the obsolescence of textbook models in which banks are at the center of a mechanistic process that multiplies the supply of money and credit. When the monetary base increases by $1 billion in these models, people deposit this $1 billion in their checking accounts; banks keep, say, 10% to satisfy their reserve requirements and lend the remaining $900 million; borrowers spend this $900 million, which is then deposited in checking accounts; and banks lend another $810 million (90% of $900 million). When the dust settles, the $1 billion increase in the monetary base has increased checking account balances by $10 billion and bank loans by $9 billion. The Fed can use the monetary base to control spending and borrowing tightly.

That’s the story and maybe it was relevant once upon a time. (And maybe Santa Claus is real, too?) Today, bank reserve requirements are minimal (they have been 0 percent since March 26, 2020) and most spending and borrowing is not through banks. Individuals and businesses can spend and borrow with credit cards, home equity loans, margin accounts, and all sorts of securities. With no effective reserve requirements on this borrowing, there is literally no limit to how much credit can be created. Think again of the textbook story of bank deposits and lending, but with no reserve requirements. If the monetary base increases by $1 billion, people deposit this $1 billion in their checking accounts; banks lend the full $1 billion; borrowers spend this $1 billion, which is then deposited in checking accounts; and banks lend another $1 billion. The dust need not ever settle!

The enormous growth in nonbank borrowing and lending has effectively obliterated the idea of a tight relationship between the monetary base and the amount of money people can borrow and the amount they have available for spending.

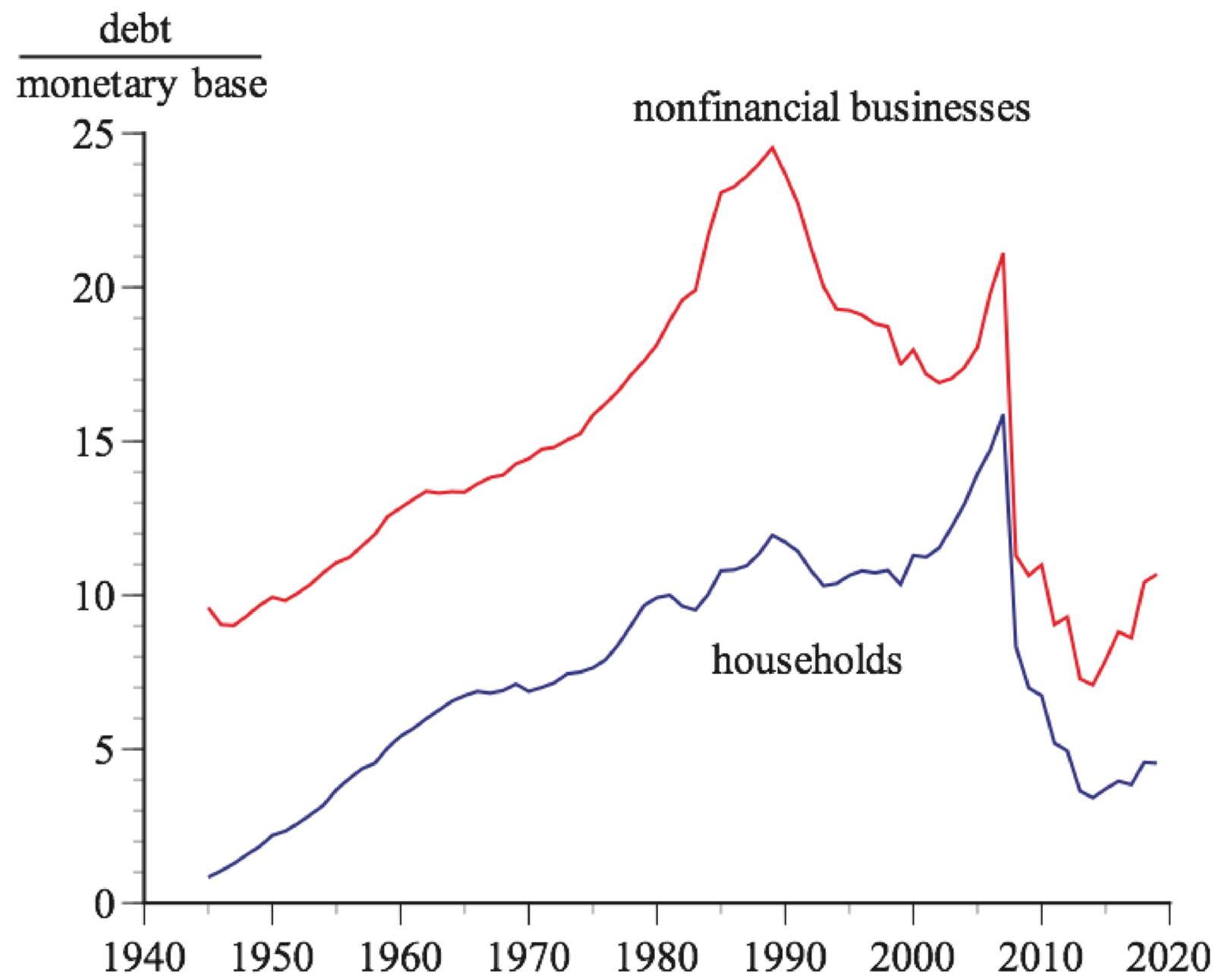

Figure 4 confirms that there is no fixed relationship between the monetary base and the debts of households and non-financial businesses. The ratio of debt to the monetary base has grown over time, collapsed, surged, and collapsed again—not at all like the constant ratio given in simple textbook models.

This doesn’t mean that the Fed is impotent. They can certainly fight recessions and cause recessions. But the modern financial system is far too complicated for there to be a close link between the money supply and inflation. We can be confident of two things. First, increases in the money supply need not cause inflation. Second, if there is ever a worrisome increase in the rate of inflation, the Fed will do whatever is needed to contain it.

Also by Gary Smith: The birds aren’t real. But maybe the surveillance is. A defense of our fundamental right to privacy. Technology can free us from drudgery but also enable surveillance that enslaves us. Then, far from computers becoming more like humans, we may become more like computers.