Detecting BS Research: If It Seems Too Good to be True…

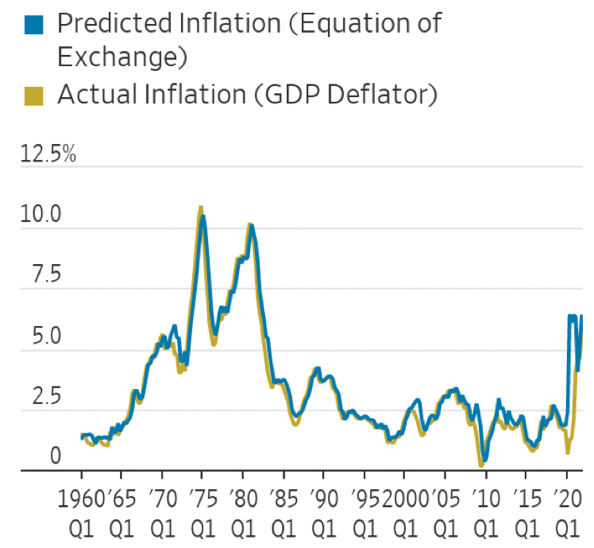

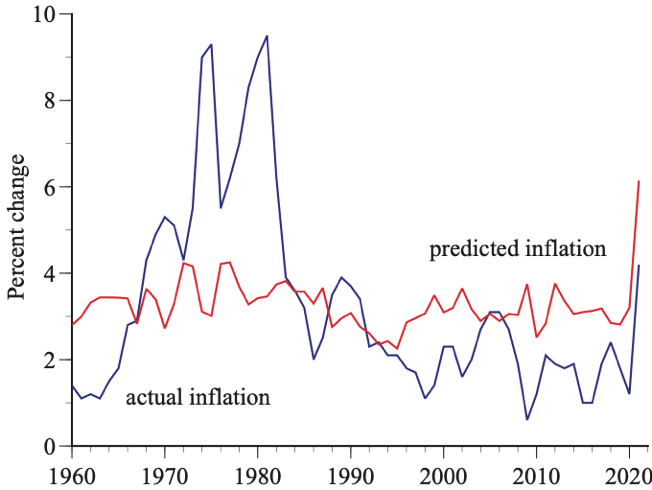

A recent Wall Street Journal article shows a near-perfect link between inflation and money. But a link that near-perfect raises suspicionsTwo Johns Hopkins economists recently wrote a Wall Street Journal opinion piece titled, “Jerome Powell Is Wrong. Printing Money Causes Inflation.” Their argument is that Federal Reserve chair Powell is mistaken in his assertions that there is not a close relationship between money and inflation. As evidence, they offer the chart below, showing that the rate of inflation can be predicted almost perfectly from the rate of increase of M2, a broad measure of money.

The authors explain:

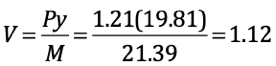

The theory rests on a simple identity, the equation of exchange, which demonstrates the link between the money supply and inflation: MV=Py, where M is the money supply, V is the velocity of money (the speed at which it circulates relative to total spending), P is the price level, and y is real gross domestic product.

Steve H. Hanke and Nicholas Hanlon, “Jerome Powell Is Wrong. Printing Money Causes Inflation.” At the Wall Street Journal

The federal government reports data on money, velocity, and GDP, and it is natural to think that these data can be used with the equation of exchange to predict prices:

The problem is that velocity is not independently measured; it is calculated from the other three variables!

For example, in the fourth quarter of 2021, the price level was 1.21, real GDP was 19.81 trillion, and M2 was 21.39 trillion; so, the government calculated velocity to be 1.12:

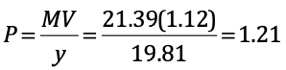

The use of this calculated velocity in the equation of exchange does not “predict” prices. All it tells us is the price that was used to calculate velocity:

The fit in the WSJ graph is nearly perfect because it is perfectly circular: prices were used to calculate velocity which was then used to calculate prices. The only slippage is the rounding errors in calculating percentage changes.

If velocity were a given constant, like the speed of light, then the circularity would be broken and inflation could be predicted from changes in the money supply and the given, fixed value of velocity. Alas, velocity is not constant and Powell is right — there is no simple relationship between money and inflation.

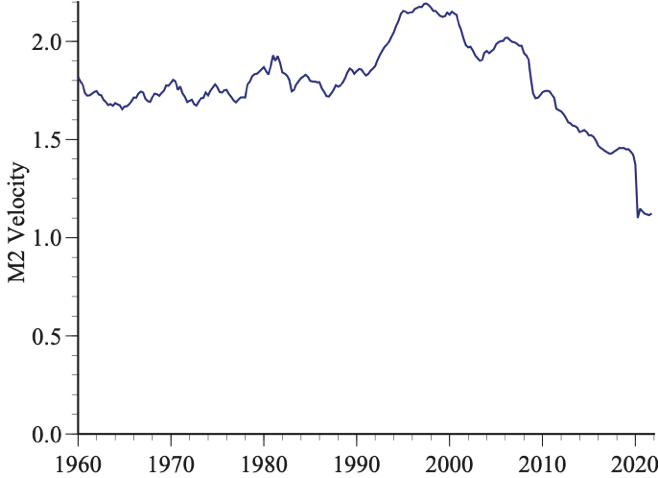

A graph of M2 velocity since 1960, the same period covered by the WSJ article, shows plenty of short-term wiggles in addition to a longer-run trend up and then down:

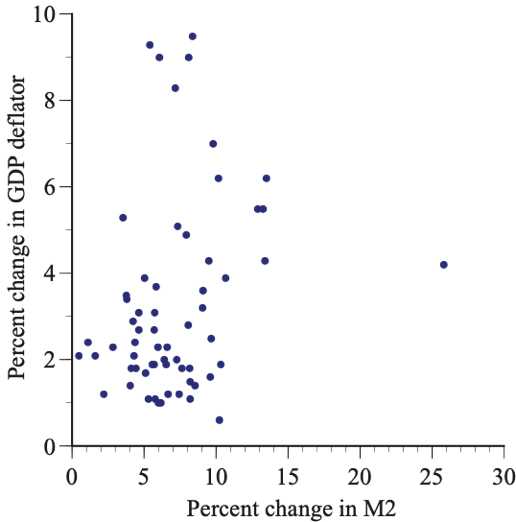

A scatterplot of annual changes in M2 and inflation (the same data used in the WSJ article) shows perhaps a positive relationship but certainly not one that could be used to predict inflation from changes in M2 reliably:

Finally, a linear regression model confirms that predicting inflation from changes in M2 is a waste of time:

I learned of this WSJ nonsense via an e-mail from Jay Cordes. Jay is not an economist, but he does know data and he knows that predictions of human behavior are never as precise as indicated in the WSJ:

Okay, I’m calling bullcrap on that chart below. No “predictions” ever match up that well with reality. What’s the trick?

The moral is that if you encounter empirical claims that are implausible (like Asian-Americans being prone to heart attacks on the fourth day of every month or hurricanes being deadlier if they have female names), or results that are too good to be true, they probably aren’t true.

Despite any fondness the WSJ editors might have for the idea that there is a close link between money and inflation, they should have been smart enough and seasoned enough to know BS when they see it. So should we all.